Discover what to expect in your first meeting with a financial adviser. Learn how to prepare, what questions to ask, and how fees work for tailored financial advice.

Discover what to expect in your first meeting with a financial adviser. Learn how to prepare, what questions to ask, and how fees work for tailored financial advice.

Discover how a suitability assessment forms the foundation of financial advice, the FCA rules behind it, and how regular reviews help keep your plan on track.

A guide to how advisers measure risk tolerance and identify client objectives as part of the suitability assessment.

Discover how financial advisers assess your financial capability, identify vulnerabilities, and tailor advice to ensure clear, confident decision‑making.

Financial planning support for life events delivered with calm, compassionate guidance. Get clear advice tailored to divorce, loss, retirement or redundancy.

Supporting vulnerable clients starts with understanding the FCA definition and offering accessible, empathetic support tailored to your needs. Download our confidential questionnaire to help start the conversation.

We explain how we use accessible communication to support vulnerable clients, including plain English, accessible formats and alternative options on request.

Find out what happens at your financial review meeting, why it matters, and how to prepare so your financial plan stays aligned with your goals.

Discover how clear, consistent financial planning communications help keep you informed, reassured and aligned with your long term goals.

Learn how

monitoring suitability over time helps to keep your financial plan aligned with your goals, circumstances and comfort with risk as life changes.

Your emergency fund should be easy to access, safe, and earning a competitive rate. Discover where to keep emergency cash savings and what to review regularly.

New details on the proposed mansion tax suggest homes above £2 million could see price pressure. Find out what the surcharge may mean for property values.

Pension access age is rising in April 2028 as the normal minimum pension age increases from 55 to 57. Learn who’s affected and how protected pension ages work.

Inflation rising is being driven by higher oil prices. Learn what’s behind the rise, why 2% inflation looks less likely, and what it could mean for households.

House prices vs inflation shows a surprise result. We compare UK house prices with CPI data over the last decade to see what homeowners really gained.

State pension age 67 is being phased in from April 2026. Find out who is affected, how the change works, and why life expectancy matters.

The OBR has raised concerns about UK tax incentives. We explain what high marginal tax rates could mean for your tax planning.

New research suggests millions of mid-lifers are not on track for retirement. Explore why and what has changed. Are you facing a retirement crisis?

New ONS data shows UK healthy life expectancy has fallen, with men and women spending fewer years in good health. Learn why the gap between lifespan and healthy lifespan matters for long term financial planning

Sales of annuities have surged, reaching £7.4bn in 2025, driven by rising annuity rates and upcoming inheritance tax changes. Explore why more people are choosing guaranteed income again.

A House of Lords committee has raised major concerns about the government’s proposed pension and IHT rules, including tight deadlines and low public awareness. Learn what the changes could mean ahead of 2027.

Millions of taxpayers overpaid income tax due to incorrect PAYE tax codes. Learn how codes are calculated and why checking yours could prevent mistakes.

Freddo inflation - prices are rising, and it reveals more about UK inflation than you’d think. A simple, fun way to understanding your pound’s real worth.

Explore how the ongoing freeze to auto-enrolment thresholds affects eligibility, pension contributions and the long term impact on retirement planning.

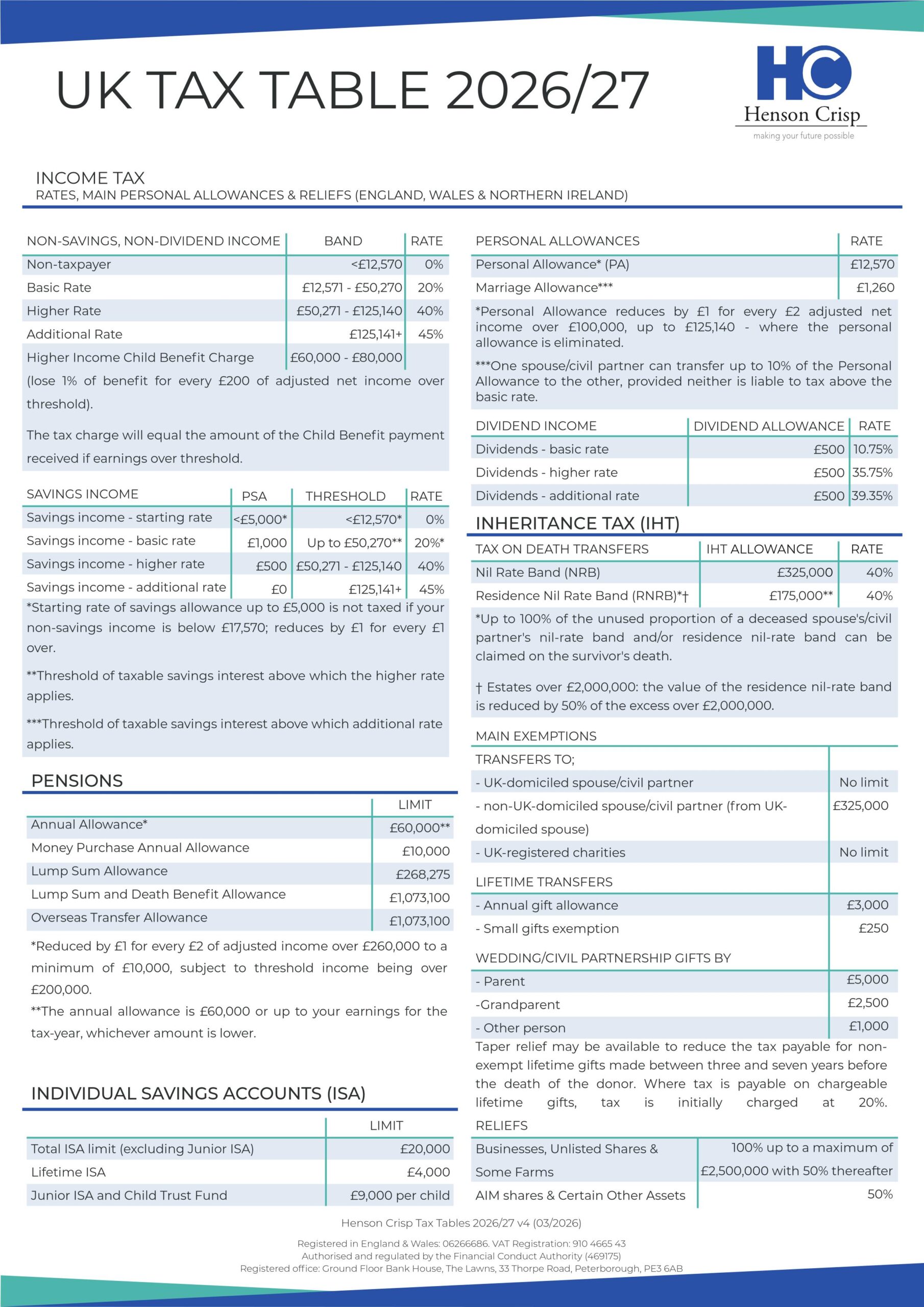

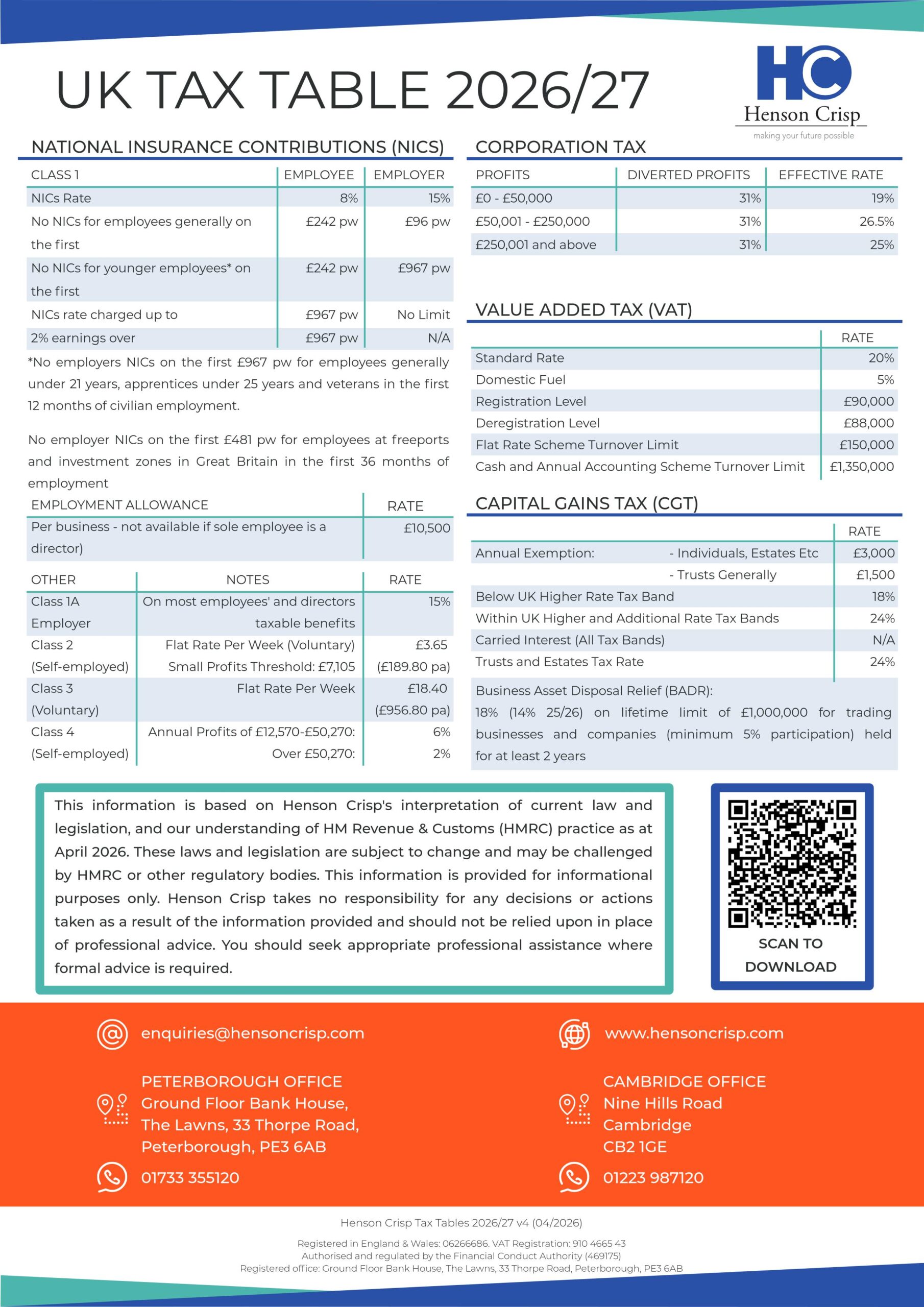

The new tax year from 6 April brings key changes to dividend tax, Making Tax Digital, inheritance tax reliefs, capital gains tax, and the State Pension Age. Here’s the expected tax and pension changes in 2026.

Making Tax Digital begins in April for many self employed and property owners. Learn who is affected, what’s required and why HMRC communication is causing confusion.

Discover why the FTSE 100 outperformed the S&P 500 in 2025, and how banks, commodities and currency shifts shaped last year’s biggest investment performance surprise.

Explore the key announcements from the Spring Forecast 2026, including updates on the UK economy, tax measures, National Insurance, wages and business changes.

Explore how UK inflation reached 3.4% in 2025, which sectors drove price changes, and what this means for planning as inflation trends shift into 2026.

Tuition fees in England are set to rise with inflation and could exceed £10,000 by 2028. Learn how new rules and Plan 5 student loans affect future students.

We’re happy to announce an exciting milestone - we’ve opened our new office in Cambridge!

Salary sacrifice rules for pensions will change in 2029, capping NIC savings. Learn what this means and how to plan ahead for maximum benefits.

The frozen income tax personal allowance could push pensioners into tax liability. Learn how the State pension and thresholds affect planning.

The Autumn Budget announced major ISA changes from April 2027, including cash limits, fund restrictions, and LISA withdrawal. Learn what’s ahead.

The Autumn Budget announced major ISA changes from April 2027, including cash limits, fund restrictions, and LISA withdrawal. Learn what’s ahead.

With the tax year ending on 5 April, explore essential year-end tax planning tips on thresholds, IHT exemptions, and marriage allowances to help maximise your savings.

The UK government quietly raised the Inheritance Tax (IHT) relief ceiling for farms and businesses to £2.5m. Here’s what it means for estate planning in 2026.

Choosing impact over tradition: this Christmas we’re donating the cost of cards to our local Trussell Trust food bank to support families who need it most.

We are excited to announce that we’re coming to Cambridge. This extension allows us to bring our trusted advice and client-first approach to even more people across the region.

Conflicting views about retirement are not unique. A new report reveals a 5-year retirement age gap between when people want to retire and when they expect to.

HMRC’s latest statistics show a jump in unclaimed Child Trust Funds (CTFs) to over £1,500,000,000.

The Autumn Statement has arrived, with speculation finally at an end, we can confirm what was announced today.

HMRC is writing to taxpayers about dividend income on 2023/24 returns. Find out what the letters mean, what to check, and how to respond.

Gold surged +47% in 2025 while the S&P 500 lagged. Discover how currency shifts reshaped ETF returns and what it means for global investors.

HMRC figures for 2023/24 show cash ISA subscriptions have increased by around 224% more than stocks and shares ISAs by the end of the decade.

The former Deputy Prime Minister Angela Rayner’s recent problems with stamp duty land tax (SDLT) offer a salutary lesson.

As the Autumn Budget approaches, government bonds are coming back into the spotlight.

A new survey has revealed a high level of public unawareness of impending pension changes and the need to plan.

The ingredients to determine next April’s increase in the State pension are now clear and suggest a problem deferred until the 2026 Budget.

Many people are wondering whether they should take their tax-free pension cash now, just in case the rules change. HMRC has issued a clear warning to be careful.

The government has published its reply to the many responses made to last October’s consultation paper on bringing pensions within the scope of inheritance tax (IHT).

Investment risk is often highlighted negatively. Discover the positive aspects of investing discussed by the Chancellor.

Investment risk is often highlighted negatively. Discover the positive aspects of investing discussed by the Chancellor.

The Bank of England cut interest rates to 4% after a rare second vote. Discover why it happened, the inflation outlook, and what it means for investors.

HMRC’s delayed salary sacrifice report sparks questions. Find out what the findings could mean for employers and pension savers alike.

The new Pension Schemes Bill could transform workplace pensions. Learn about small pot consolidation, private market investments and more.

The Winter Fuel Payment is back for most pensioners in England and Wales. Find out who qualifies and how income limits affect eligibility.

Pension funds may be steered toward UK investments under the Mansion House Accord. Discover how this affects your retirement planning.

UK CPI rose to 3.5% in April 2025. Find out what’s driving inflation and how it could impact your retirement and financial plans.

New research reveals Gen Z, low earners, and the self-employed face high risk of retirement poverty. Learn how to protect your future savings today.

Gold prices surged in early 2025 amid tariff fears. Find out what caused the chaos in the gold market and what it means for investors today.

Rising interest rates mean more savers now owe tax on savings interest. HMRC warns taxpayers to act, as PSA limits remain frozen.

2025 marks the 50th anniversary of a momentous yet often overlooked event in UK tax history — the last time a Chancellor introduced a basic income tax increase.

Major State Pension Age changes are approaching, yet many remain unaware. Find out if you’re affected and how to plan ahead.

Chancellor Reeves has reversed the Winter Fuel Payment cuts. Around 9 million pensioners will receive up to £300 towards energy bills in 2025.

Trump’s tariffs unsettled markets and US Treasuries. Find out why bond markets matter and what investors should take from it.

The latest UK life expectancy data from the ONS and what it means for State Pension Age changes. How will it impact future retirement plans.

The House of Commons Treasury Committee has been pondering the future of Lifetime ISAs (LISAs).

The government is showing no signs of changing its plans to levy inheritance tax (IHT) on pensions.

There were no tax increases in the Chancellor’s Spring Statement (upgraded from an initial Spring Forecast), but that might just be pain deferred.

The government has confirmed that there will be no revisions to automatic enrolment in workplace pensions for 2025/26.

2025’s first set of inflation numbers were higher than expected, but more rises are coming.

The start of the new tax year warrants as much planning as the end of the old tax year.

Chancellor Rachel Reeves delivered the Spring Statement 2025, outlining the UK’s economic outlook and the government’s fiscal priorities.

Inflation fell in 2024, dropping to 2.5% from 4.0% in 2023. So why didn’t it feel like that?

One of the world’s largest investment managers, BlackRock, recently published its latest review of the UK’s retirement landscape.

The impact of the Budget’s increases in national insurance contributions (NICs) are not limited to employers.

Inflation fell in 2024, dropping to 2.5% from 4.0% in 2023. So why didn’t it feel like that?

National Savings & Investments (NS&I) has been busy reducing its interest rates in recent months.

There are now over three million 'lost' pensions worth over £31 billion. Could you have lost a pension somewhere?

As 2025 gets under way, it is once again the time of year to start considering your year-end tax planning.

The latest Budget move to count pensions as part of your estate for inheritance tax (IHT) is a major change, with potentially significant consequences.

HMRC is uncharacteristically keen to give money away, reminding young adults again that they may be due unclaimed child trust funds (CTFs).

A third deadline for topping up State Pension entitlement is now coming into view.

New statistics show that cash ISAs remain a popular investment. The latest information relates to the tax year 2022/23.

The Institute for Fiscal Studies (IFS) has been crunching the numbers on the adequacy of pension contributions.

Financial Conduct Authority (FCA) publishes a review of the cash savings market following evidence of some dubious tactics at work.

We’re incredibly proud to announce that Henson Crisp has been recognised in the NMA Top 100 Independent Financial Adviser (IFA) firms in the UK by New Model Adviser.

We now have a clear understanding of how much the main State Pension will increase next April.

Investors in cryptocurrencies like bitcoin should not forget the tax consequences of their digital wallets, says HMRC.

The Autumn Statement, Labour’s first in over 14 years and referred to as the “Mega Budget,” has been released.

The Personal Savings Allowance determines how much interest you can earn on your savings before being liable to pay any tax.

Many chancellors ago, in November 2016, Philip Hammond announced an end to spring Budgets and their replacement with autumn Budgets.

Will increased capital gains tax (CGT) mean less tax gets paid?

Carma aims to make a positive social and environmental impact – through tree planting.

2022 was an eventful year, giving you good reason to think about your financial planning for 2023.

Why not consider a different kind of gift for your children or grandchildren this Christmas – perhaps one with a financial twist?

We regularly donate to many charities, in addition to supporting several local organisations.

Last night Henson Crisp attended the Peterborough Telegraph’s Business Excellence Awards as a finalist in the Small Business of the Year category.

The Autumn Statement 2022 has caused a stir for businesses, employees and individuals. So let’s take a look at the upcoming changes and break down some key points that may affect you.

The rapid unwinding of most of September’s so-called mini-budget has important implications.

On 14 October, as an important deadline loomed for Bank of England support of the government bond markets to expire, the government’s political turmoil ratcheted up as the fallout from the ‘fiscal event’ of 23 September claimed its first scalp.

Celebrating its 15th year of trading, Henson Crisp now advises on close to £150m of assets for 130 families. To continue the growth of the business two new directors have been appointed.

We are hearing this a lot recently, not only because it is on the FCA’s agenda and COP26 but because it is becoming more important to us and the future of our society.

Henson Crisp, proud local sponsors of Triceratops, as The Natural History Museum brings its touring exhibition of Dinosaurs to Peterborough Cathedral this summer!

Pension access age is rising in April 2028 as the normal minimum pension age increases from 55 to 57. Learn who’s affected and how protected pension ages work.

State pension age 67 is being phased in from April 2026. Find out who is affected, how the change works, and why life expectancy matters.

The OBR has raised concerns about UK tax incentives. We explain what high marginal tax rates could mean for your tax planning.

New research suggests millions of mid-lifers are not on track for retirement. Explore why and what has changed. Are you facing a retirement crisis?

New ONS data shows UK healthy life expectancy has fallen, with men and women spending fewer years in good health. Learn why the gap between lifespan and healthy lifespan matters for long term financial planning

Sales of annuities have surged, reaching £7.4bn in 2025, driven by rising annuity rates and upcoming inheritance tax changes. Explore why more people are choosing guaranteed income again.

A House of Lords committee has raised major concerns about the government’s proposed pension and IHT rules, including tight deadlines and low public awareness. Learn what the changes could mean ahead of 2027.

Explore how the ongoing freeze to auto-enrolment thresholds affects eligibility, pension contributions and the long term impact on retirement planning.

The new tax year from 6 April brings key changes to dividend tax, Making Tax Digital, inheritance tax reliefs, capital gains tax, and the State Pension Age. Here’s the expected tax and pension changes in 2026.

Salary sacrifice rules for pensions will change in 2029, capping NIC savings. Learn what this means and how to plan ahead for maximum benefits.

A new survey has revealed a high level of public unawareness of impending pension changes and the need to plan.

The ingredients to determine next April’s increase in the State pension are now clear and suggest a problem deferred until the 2026 Budget.

Many people are wondering whether they should take their tax-free pension cash now, just in case the rules change. HMRC has issued a clear warning to be careful.

HMRC’s delayed salary sacrifice report sparks questions. Find out what the findings could mean for employers and pension savers alike.

The new Pension Schemes Bill could transform workplace pensions. Learn about small pot consolidation, private market investments and more.

Pension funds may be steered toward UK investments under the Mansion House Accord. Discover how this affects your retirement planning.

New research reveals Gen Z, low earners, and the self-employed face high risk of retirement poverty. Learn how to protect your future savings today.

Major State Pension Age changes are approaching, yet many remain unaware. Find out if you’re affected and how to plan ahead.

The latest UK life expectancy data from the ONS and what it means for State Pension Age changes. How will it impact future retirement plans.

The government is showing no signs of changing its plans to levy inheritance tax (IHT) on pensions.

The government has confirmed that there will be no revisions to automatic enrolment in workplace pensions for 2025/26.

One of the world’s largest investment managers, BlackRock, recently published its latest review of the UK’s retirement landscape.

There are now over three million 'lost' pensions worth over £31 billion. Could you have lost a pension somewhere?

As 2025 gets under way, it is once again the time of year to start considering your year-end tax planning.

The latest Budget move to count pensions as part of your estate for inheritance tax (IHT) is a major change, with potentially significant consequences.

A third deadline for topping up State Pension entitlement is now coming into view.

The Institute for Fiscal Studies (IFS) has been crunching the numbers on the adequacy of pension contributions.

We now have a clear understanding of how much the main State Pension will increase next April.

Your emergency fund should be easy to access, safe, and earning a competitive rate. Discover where to keep emergency cash savings and what to review regularly.

New details on the proposed mansion tax suggest homes above £2 million could see price pressure. Find out what the surcharge may mean for property values.

Millions of taxpayers overpaid income tax due to incorrect PAYE tax codes. Learn how codes are calculated and why checking yours could prevent mistakes.

The new tax year from 6 April brings key changes to dividend tax, Making Tax Digital, inheritance tax reliefs, capital gains tax, and the State Pension Age. Here’s the expected tax and pension changes in 2026.

Making Tax Digital begins in April for many self employed and property owners. Learn who is affected, what’s required and why HMRC communication is causing confusion.

Tuition fees in England are set to rise with inflation and could exceed £10,000 by 2028. Learn how new rules and Plan 5 student loans affect future students.

The frozen income tax personal allowance could push pensioners into tax liability. Learn how the State pension and thresholds affect planning.

With the tax year ending on 5 April, explore essential year-end tax planning tips on thresholds, IHT exemptions, and marriage allowances to help maximise your savings.

The former Deputy Prime Minister Angela Rayner’s recent problems with stamp duty land tax (SDLT) offer a salutary lesson.

As the Autumn Budget approaches, government bonds are coming back into the spotlight.

The ingredients to determine next April’s increase in the State pension are now clear and suggest a problem deferred until the 2026 Budget.

The government has published its reply to the many responses made to last October’s consultation paper on bringing pensions within the scope of inheritance tax (IHT).

Rising interest rates mean more savers now owe tax on savings interest. HMRC warns taxpayers to act, as PSA limits remain frozen.

2025 marks the 50th anniversary of a momentous yet often overlooked event in UK tax history — the last time a Chancellor introduced a basic income tax increase.

The government is showing no signs of changing its plans to levy inheritance tax (IHT) on pensions.

The start of the new tax year warrants as much planning as the end of the old tax year.

As 2025 gets under way, it is once again the time of year to start considering your year-end tax planning.

Investors in cryptocurrencies like bitcoin should not forget the tax consequences of their digital wallets, says HMRC.

The Personal Savings Allowance determines how much interest you can earn on your savings before being liable to pay any tax.

Will increased capital gains tax (CGT) mean less tax gets paid?

Your emergency fund should be easy to access, safe, and earning a competitive rate. Discover where to keep emergency cash savings and what to review regularly.

Discover why the FTSE 100 outperformed the S&P 500 in 2025, and how banks, commodities and currency shifts shaped last year’s biggest investment performance surprise.

Gold surged +47% in 2025 while the S&P 500 lagged. Discover how currency shifts reshaped ETF returns and what it means for global investors.

HMRC figures for 2023/24 show cash ISA subscriptions have increased by around 224% more than stocks and shares ISAs by the end of the decade.

As the Autumn Budget approaches, government bonds are coming back into the spotlight.

Investment risk is often highlighted negatively. Discover the positive aspects of investing discussed by the Chancellor.

Investment risk is often highlighted negatively. Discover the positive aspects of investing discussed by the Chancellor.

Gold prices surged in early 2025 amid tariff fears. Find out what caused the chaos in the gold market and what it means for investors today.

Trump’s tariffs unsettled markets and US Treasuries. Find out why bond markets matter and what investors should take from it.

The House of Commons Treasury Committee has been pondering the future of Lifetime ISAs (LISAs).

National Savings & Investments (NS&I) has been busy reducing its interest rates in recent months.

New statistics show that cash ISAs remain a popular investment. The latest information relates to the tax year 2022/23.

Financial Conduct Authority (FCA) publishes a review of the cash savings market following evidence of some dubious tactics at work.

Investors in cryptocurrencies like bitcoin should not forget the tax consequences of their digital wallets, says HMRC.

New details on the proposed mansion tax suggest homes above £2 million could see price pressure. Find out what the surcharge may mean for property values.

State pension age 67 is being phased in from April 2026. Find out who is affected, how the change works, and why life expectancy matters.

A House of Lords committee has raised major concerns about the government’s proposed pension and IHT rules, including tight deadlines and low public awareness. Learn what the changes could mean ahead of 2027.

Explore the key announcements from the Spring Forecast 2026, including updates on the UK economy, tax measures, National Insurance, wages and business changes.

Salary sacrifice rules for pensions will change in 2029, capping NIC savings. Learn what this means and how to plan ahead for maximum benefits.

The frozen income tax personal allowance could push pensioners into tax liability. Learn how the State pension and thresholds affect planning.

The Autumn Budget announced major ISA changes from April 2027, including cash limits, fund restrictions, and LISA withdrawal. Learn what’s ahead.

The Autumn Budget announced major ISA changes from April 2027, including cash limits, fund restrictions, and LISA withdrawal. Learn what’s ahead.

HMRC’s latest statistics show a jump in unclaimed Child Trust Funds (CTFs) to over £1,500,000,000.

The Autumn Statement has arrived, with speculation finally at an end, we can confirm what was announced today.

HMRC is writing to taxpayers about dividend income on 2023/24 returns. Find out what the letters mean, what to check, and how to respond.

The former Deputy Prime Minister Angela Rayner’s recent problems with stamp duty land tax (SDLT) offer a salutary lesson.

As the Autumn Budget approaches, government bonds are coming back into the spotlight.

HMRC’s delayed salary sacrifice report sparks questions. Find out what the findings could mean for employers and pension savers alike.

The new Pension Schemes Bill could transform workplace pensions. Learn about small pot consolidation, private market investments and more.

The Winter Fuel Payment is back for most pensioners in England and Wales. Find out who qualifies and how income limits affect eligibility.

Pension funds may be steered toward UK investments under the Mansion House Accord. Discover how this affects your retirement planning.

Rising interest rates mean more savers now owe tax on savings interest. HMRC warns taxpayers to act, as PSA limits remain frozen.

2025 marks the 50th anniversary of a momentous yet often overlooked event in UK tax history — the last time a Chancellor introduced a basic income tax increase.

Chancellor Reeves has reversed the Winter Fuel Payment cuts. Around 9 million pensioners will receive up to £300 towards energy bills in 2025.

Trump’s tariffs unsettled markets and US Treasuries. Find out why bond markets matter and what investors should take from it.

There were no tax increases in the Chancellor’s Spring Statement (upgraded from an initial Spring Forecast), but that might just be pain deferred.

The government has confirmed that there will be no revisions to automatic enrolment in workplace pensions for 2025/26.

Chancellor Rachel Reeves delivered the Spring Statement 2025, outlining the UK’s economic outlook and the government’s fiscal priorities.

The impact of the Budget’s increases in national insurance contributions (NICs) are not limited to employers.

HMRC is uncharacteristically keen to give money away, reminding young adults again that they may be due unclaimed child trust funds (CTFs).

The Autumn Statement, Labour’s first in over 14 years and referred to as the “Mega Budget,” has been released.

Many chancellors ago, in November 2016, Philip Hammond announced an end to spring Budgets and their replacement with autumn Budgets.

A House of Lords committee has raised major concerns about the government’s proposed pension and IHT rules, including tight deadlines and low public awareness. Learn what the changes could mean ahead of 2027.

With the tax year ending on 5 April, explore essential year-end tax planning tips on thresholds, IHT exemptions, and marriage allowances to help maximise your savings.

The UK government quietly raised the Inheritance Tax (IHT) relief ceiling for farms and businesses to £2.5m. Here’s what it means for estate planning in 2026.

The government has published its reply to the many responses made to last October’s consultation paper on bringing pensions within the scope of inheritance tax (IHT).

The government is showing no signs of changing its plans to levy inheritance tax (IHT) on pensions.

Inflation fell in 2024, dropping to 2.5% from 4.0% in 2023. So why didn’t it feel like that?

As 2025 gets under way, it is once again the time of year to start considering your year-end tax planning.

The latest Budget move to count pensions as part of your estate for inheritance tax (IHT) is a major change, with potentially significant consequences.

Inflation rising is being driven by higher oil prices. Learn what’s behind the rise, why 2% inflation looks less likely, and what it could mean for households.

House prices vs inflation shows a surprise result. We compare UK house prices with CPI data over the last decade to see what homeowners really gained.

Freddo inflation - prices are rising, and it reveals more about UK inflation than you’d think. A simple, fun way to understanding your pound’s real worth.

Explore how UK inflation reached 3.4% in 2025, which sectors drove price changes, and what this means for planning as inflation trends shift into 2026.

Tuition fees in England are set to rise with inflation and could exceed £10,000 by 2028. Learn how new rules and Plan 5 student loans affect future students.

The Bank of England cut interest rates to 4% after a rare second vote. Discover why it happened, the inflation outlook, and what it means for investors.

UK CPI rose to 3.5% in April 2025. Find out what’s driving inflation and how it could impact your retirement and financial plans.

2025’s first set of inflation numbers were higher than expected, but more rises are coming.

Inflation fell in 2024, dropping to 2.5% from 4.0% in 2023. So why didn’t it feel like that?