The Autumn Budget at the end of November announced important changes to come for individual savings accounts (ISAs) from April 2027, but you may not be affected.

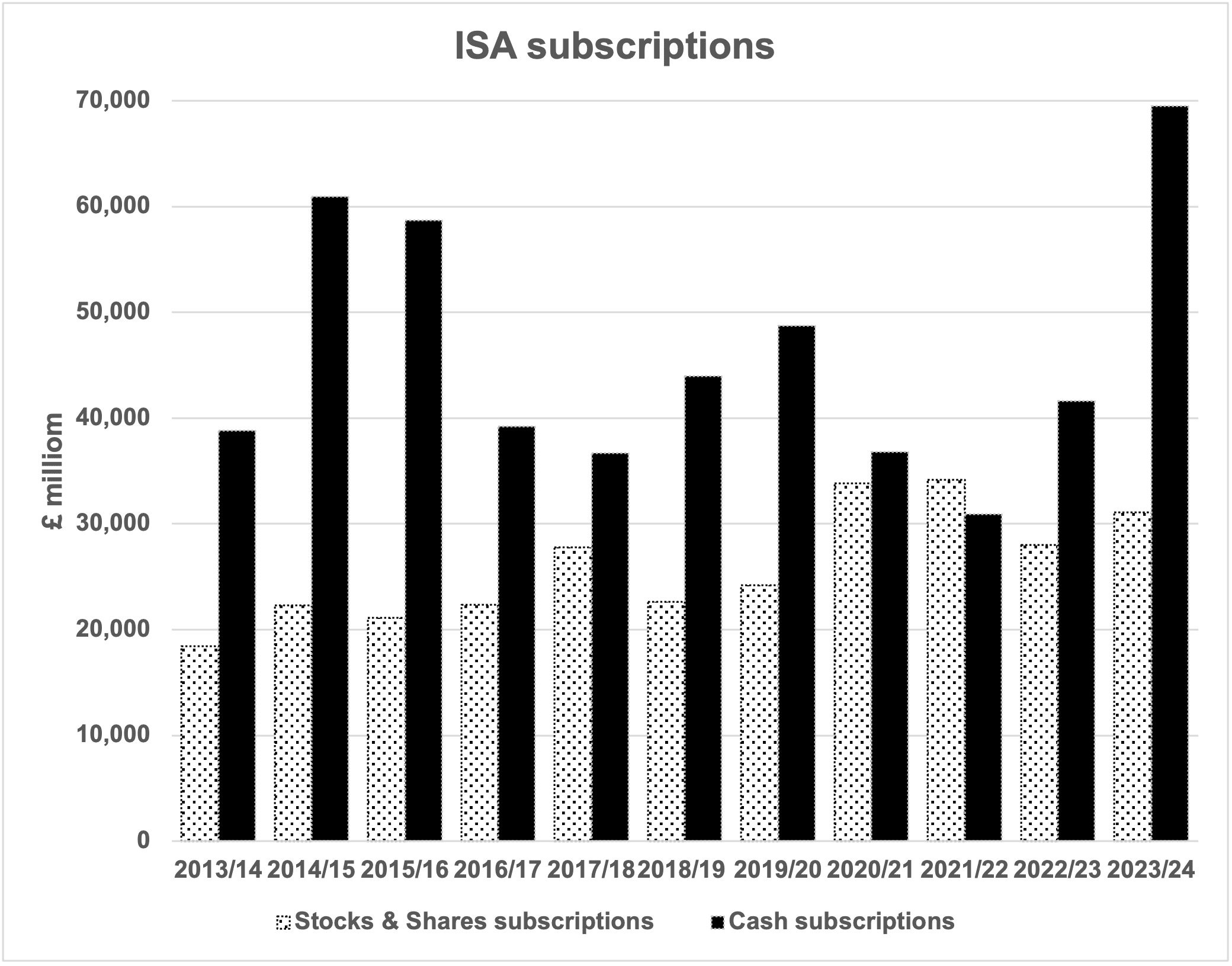

Source: HMRC

WHY THE AUTUMN BUDGET MATTERS FOR ISA SAVERS

November’s Budget announced a range of changes to ISAs, the full extent of which did not become clear immediately. While the Office for Budget Responsibility (OBR) managed to publish its primary document before the Chancellor spoke, HMRC and the Treasury were slow in releasing information through to the end of Budget week.

KEY ISA CHANGES ANNOUNCED:

The main ISA details, as we now know them, are:

• The yearly subscription limits (£20,000 overall for an adult ISA, £9,000 for a Junior ISA and £4,000 for a Lifetime ISA) will be frozen until April 2031. The adult ISA limit was last increased in April 2017, meaning the freeze will last (at least) 14 years.

• From April 2027, the maximum subscription to a cash ISA will be £12,000 for under-65 year olds. Those aged 65 and over can still subscribe to their full £20,000 cash ISA allowance.

RESTRICTIONS ON STOCKS AND SHARES ISAS

• Also from April 2027, there will be new restrictions on the funds that can be held in stocks and shares ISAs by the under-65s. These will be designed to exclude ‘cash-like’ funds, such as money market funds. It is unclear whether these restrictions will only apply to new subscriptions or also cover existing investments.

• When the new restrictions begin, any interest earned on cash held in stocks and shares ISAs by under-65s will be subject to a charge, currently unspecified.

LIFETIME ISA WITHDRAWAL AND NEW FIRST-TIME BUYER ISA

• A consultation paper will be published soon on the design of a new ISA to support first-time buyers saving for a deposit. Once this new ISA becomes available, the Lifetime ISA (LISA) will be withdrawn. It is unclear whether subscriptions to existing LISAs will then have to stop, but precedent suggests otherwise.

WHAT THESE CHANGES MEAN FOR SAVERS

These changes are largely a reversion to the past ISA formats. The revised treatment of cash ISAs echoes the situation before July 2014, when the cash subscription limit was half of the overall maximum and interest received in a stocks and shares ISA suffered a 20% charge. Similarly, until December 2019 when it was replaced by the LISA, there was a Help to Buy ISA.

As the tax year end approaches, if you are thinking of investing in an ISA, make sure you get advice about how the planned changes could affect your choice of plan.