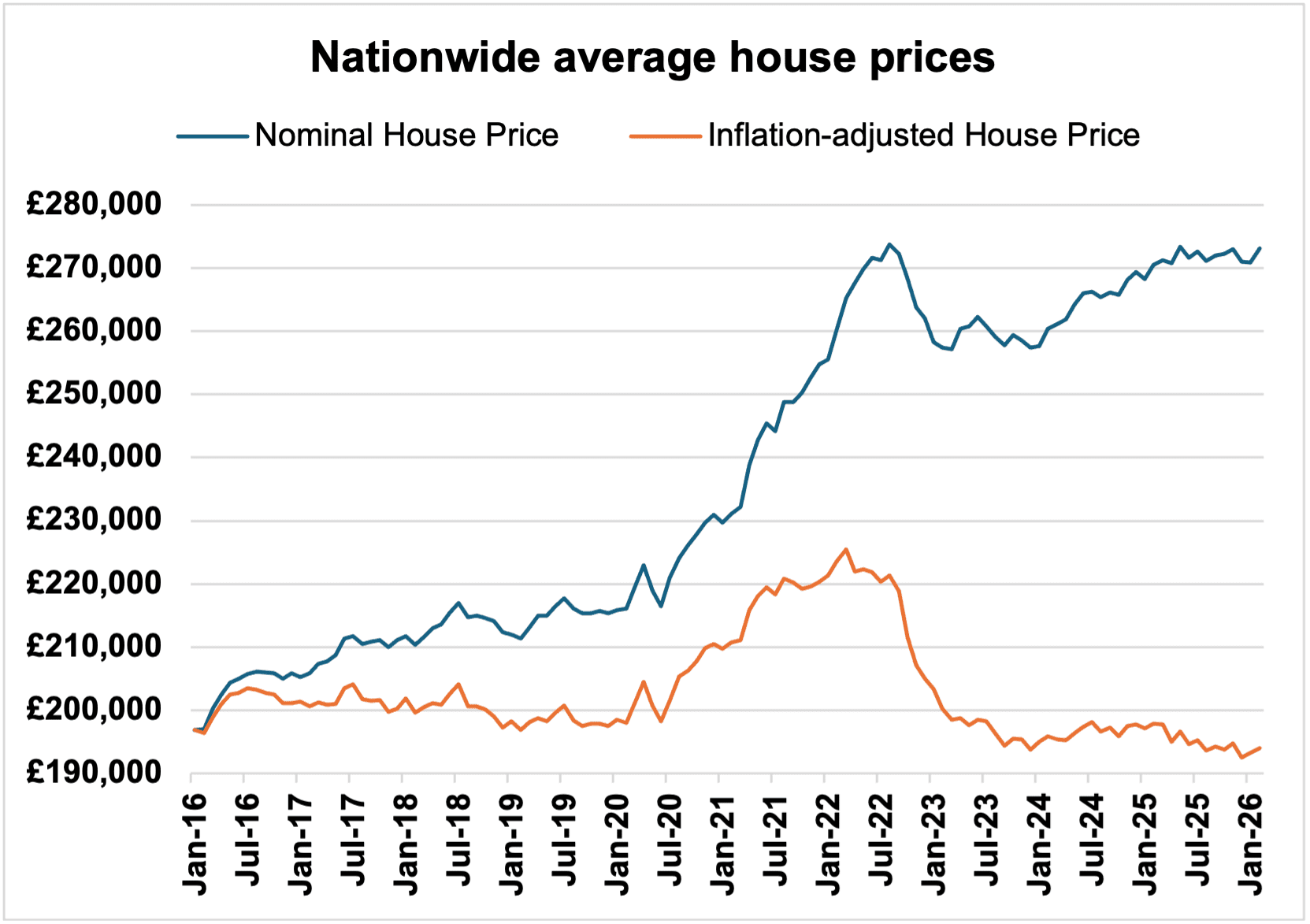

What the data shows about house prices vs inflation

Nationwide Building Society says the average UK house price in January 2016 was £196,829. Ten years later, it had risen to £270,873, a 37.6% increase. Over the same period, the Consumer Prices Index (CPI) increased by 40.2%.

The house price growth has slowed

If the result is not what you expected, it could be because you remember the unexpected boom during and immediately after the Covid-19 pandemic, but forgot the somewhat turgid period for house prices that followed. In the three years from January 2023, the average house price rose by 4.9%, while the CPI added 10.4%.

The impact of interest rates on property

Ironically, some of the recent slowdown in house price growth is linked to general inflation. One factor that put the brake on house prices was the increase in interest rates made by the Bank of England to bring down inflation (which peaked at over 11% in October 2022). Until June 2022, the Bank of England rate was no more than 1%. As anyone facing the imminent expiry of a five-year fixed rate mortgage knows, the Bank’s action on interest rates, now compounded by the Iran war, has made borrowing considerably more expensive than half a decade ago.

Buy-to-let pressures and rental demand

The near flatlining of house prices and, until recently, cuts to mortgage rates did make life marginally easier for first-time homebuyers. That has not been good news for one group of existing property owners: buy-to-let investors. Zoopla, the property website, reported that at the start of the year, average enquiries per rental property were at their lowest level since 2019 and down a fifth on January 2025. Reduced demand has translated into slowing rental growth, which has come down from 7.8% annual growth in January 2025 to 3.1% a year later, according to data from the Office for National Statistics. In England, buy-to-let investors are also facing the implementation of the Renters’ Rights Act, which from 1 May 2026 will put an end to no-fault evictions (‘section 21 orders’).

Buying and owning your own home generally remains a sensible move, but be wary of treating it as the only investment you need to make.