Further details have emerged about the potential impact of the ‘mansion tax’ announced in the last Budget.

Rachel Reeves’ first two Budgets have so far featured announcements of tax-raising measures with delayed starting dates. For example, the controversial changes to inheritance tax (IHT) business and agricultural relief emerged in October 2024 but have only just taken effect. Similarly, bringing pensions within the scope of IHT was announced at the same time, but will not commence until 6 April 2027.

What is the proposed mansion tax?

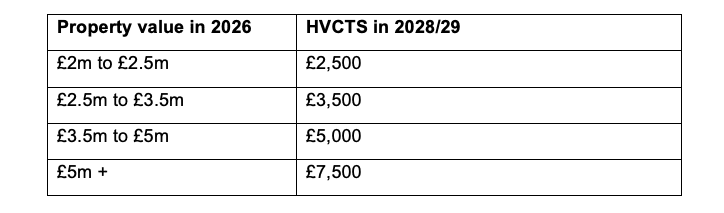

In her Autumn 2025 Budget, she set out plans for a High Value Council Tax Surcharge (HVCTS – aka ‘mansion tax’) on homes valued at £2 million and above, to start in April 2028. There was little detail about the measure, but a consultation was promised “in the New Year”. So far, nothing has been published by the Treasury, but just before Easter, the Office for Budget Responsibility (OBR) set out its assessment of the new tax’s impact. These included some interesting nuggets:

How the mansion tax could affect property prices

By 2028, the OBR thought the full value of the future HVCTS liability would be reflected in property prices. Although the OBR did not spell out the numbers, what this means in practice is that for every £1,000 of consumer price index (CPI)-linked HVCTS annual charge, the OBR expects a property’s value to drop by about £35,000. For the lowest £2,500 charge covering properties valued at £2–2.5 million, their value would drop by about £87,500, according to OBR theory.

Why high-value homes may face price pressure

The OBR forecasts that there will be a bunching of prices just below each threshold, which would further lower prices for properties that would otherwise be just above a threshold. The OBR is on solid ground with this assumption, as it is exactly what happened when a single stamp duty rate was based on a house’s price.

Appeals could be more common than expected

One-in-five property owners (who are liable to the tax, rather than the occupiers) are expected to lodge an appeal, with a 40% success rate.

Perhaps the most telling point is that the new tax would initially raise only £400 million in 2028/29, hardly even a rounding error in Treasury accounting terms. Almost the same sum could have been generated by raising the standard rate of VAT from 20% to 20.04%, although the politics would have been much trickier.

We’ll have to wait and see if the OBR’s expectations pan out.