How auto-enrolment has evolved since 2012

The narrative highlighting government success stories seems thin on the ground these days. However, one initiative that started under the previous Labour government, and was implemented by the Conservative government that followed, can count as a genuine success: automatic enrolment in workplace pensions (AE for short). The latest data shows that there are now over 22 million people in workplace pensions, an increase of more than 10 million since AE was introduced in October 2012.

why earnings threshold freezes matter

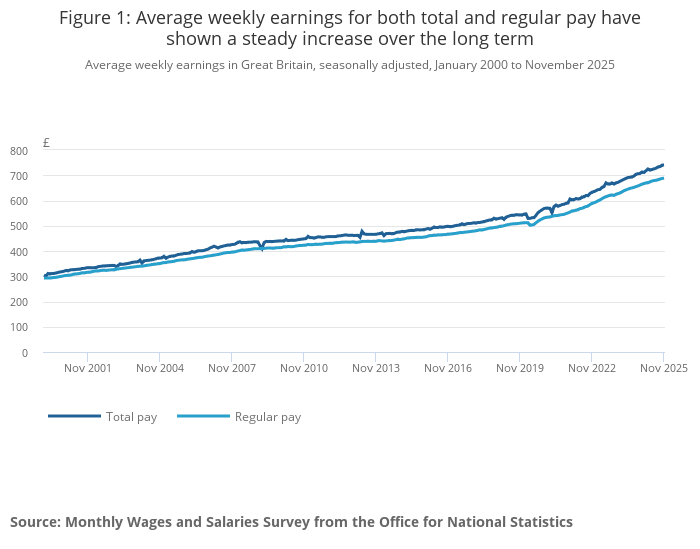

When AE started life, broadly speaking, any worker (other than the self-employed) fell within its scope if they were earning at least £8,105 a year. Once that threshold was crossed, employer and employee pension contributions were based on earnings in a band between £5,564 and £42,475. Since AE’s 2012 start date, average weekly earnings have risen by about 60%, according to the Office for National Statistics. You might, therefore, expect that the key AE earnings numbers have increased correspondingly, implying an earnings threshold of about £13,000 and an earnings band between roughly £8,900 and £68,000.

Thresholds and earnings bands in 2025/26 and 2026/27

That is not the case. For 2025/26 and 2026/27:

• The earnings threshold is £10,000, unchanged since 2014/15.

• The lower limit of the earnings band is £6,240, unchanged since 2020/21.

• The upper limit of the earnings band is £50,270, unchanged since 2021/22.

why low earning are affected differently

There is a case to be made for the freeze in the earnings threshold, as it increases eligibility among part-time earners. However, those low earners would be entitled to a state pension of £12,548 in 2026/27 (assuming, at least, a 35-year record of National Insurance Contributions), so at the bottom end they could have more income in retirement than while working.

higher earners and the shrinking pension band

The effective shrinkage in the earnings band is harder to justify. In 2012, the upper limit was about 175% of average earnings, whereas it is now around 130%. The effect is to leave higher earners with proportionately less pension coverage. The government’s argument is that: “These higher earners…are more likely to make personal arrangements for additional saving”.

what this means for pension planning

In other words, if you fall into that ‘higher earner’ category, you need to look beyond the contributions that AE mandates on you and your employer.

If you would like more information on how any of these changes could affect you, please get in touch.